Unable to Understand Market Trend as it moves from Sideways to Trending or

Is it your system or strategy? You are not having the Right Strategy and Losing

You — By repeating the same mistakes again and again

As per my experience with trading over 12+ years and also talking with 1000’s of traders over a period of time, my understating is

Traders are often their own worst enemies. The simple reason being most of the traders after doing a big loss will turn to charts and try to find their mistake. What I missed in catching this move, should I apply more indicators or should I learn something new to catch big moves etc. Readers can go back to thought process they went once they took a big loss or missed a major rally.

It’s easier to look at charts and imagine what the market might do or find an excuse , compared to turning inward and engaging in self-examination to determine if any changes in your approach to trading are required.

A very simple exercise will make you understand this

Go back to your past traders, highlight the trades where you made maximum losses, analyse all the loss making trades. You will observe over a period of time you have repeated the same mistake again and again. Be It taking an impulsive trade, trying to find top or bottom, not putting SL , taking over-sized position etc.

What would happen if you identified a recurring mistake? Would you do anything differently while trading, as a result? Would you need or use some type of structure or process to assist you in not repeating the same mistake?

The only thing we actually have any control over is our behaviour. The market will do what it will do. If one is truly interested in maximising / improving P&L, then focus on not to repeat your mistakes again. We may not be able to control our emotions, but we can learn to manage them. Trading Journal is one of the tools which can help you in understanding your mistakes and over a period of time not repeating them.

We have seen a lot of articles on the Golden Cross on various media.

Let us quickly look at how the Nifty movements have been in the last 10-12 years post the Golden Cross.

Conclusion – It’s a very late indicator but may sometimes give real long-term trend changes. Tough to use it as a decision system. The whipsaws hurt real bad. I would rather prefer looking at price patterns.

This is a quick video. Do put in your comments. Maybe next time would try to put it on Dow Jones / S&P 500

This is a blog post by Mastermind, Nooresh. The original post appears here.

One can understand the obsession for Day Trading by just doing a Search on Google for the Words like – Day Trading, Intraday Trading Tips, Day Trading Tips and the number of sites that pop up catering to it.

BSE, an exchange in India, mentions itself to be the fastest exchange in the world.

Nifty 50 index is world’s most actively traded derivatives contract: Survey – Link

Majority of brokers have 90 – 96% of their business coming from Derivatives

There are a bunch of Discount Brokers with Rs. 0-20 as broking change.

The original post is by Mastermind, Sana Securities, authored by Rajat Sharma and appears here.

I wasn’t really sure of the title to this post but the idea stemmed out of a question that I received from a subscriber.

Instead of repeating the exact question, I will break it up into 2:

Can you earn fixed interest income on the spare cash lying in your trading account?

Should you transfer spare cash into your bank account where you can earn up to 4% – 6% interest (savings account rate for Yes Bank and Kotak Mahindra Bank) or can you earn higher?

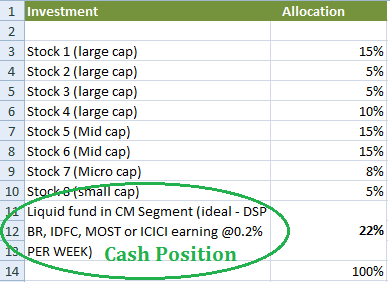

Cash Position: The best cash position is naturally the one that earns the highest possible ‘fixed income rate’ in the market. Fixed interest income can be earned on – money lying in savings/ current account, money market and liquid funds, ultra-short and short term funds and medium and long term funds.

As a trader or as a short term investor, you will require the money that you keep in your trading account at a short notice. For this reason, many short term investors believe that the best thing to do is to transfer funds from trading account to your savings bank account, perhaps at the end of the trading day (i.e. at 3.30 pm) and allocate them back to your trading account terminal when needed. It’s all in real time with internet banking these days. This is not the best thing to do.

How much are you going to earn by doing this?

Savings bank interest: In the most aggressive (bank) scenario you will earn ~ 0.06% on a weekly basis (i.e. ~ half of 6% divided by 52 weeks; considering that you transfer it exactly at 3.30 pm each day for until when the market opens on the next day).

Now consider a Liquid fund on the Mutual Fund Segment within your trading terminal.

Liquid and money market fund interest: Typically, these funds earn between 7.8% – 7.9% annual interest but that’s not all. You can actually stay invested in these funds unless you need to settle a trade (see example below). Here you will earn ~ 0.15% on a weekly basis (i.e. 5.8% divided by 52 weeks; see example below).

Example: You have Rs. 2,00,000 lying unutilised in your trading account and do not want to buy anything or make any position. You can either transfer this money to your bank account or buy a money market or liquid fund which typically earns 7.8 % return with very little volatility.

If you have stocks lying in your demat account, you will typically get 4 times their market price as margin to trade / invest (i.e. if you have stocks with current market value of Rs. 2,50,000 in your demat account, you will be allowed to buy/sell for up to Rs. 10,00,000/-). No interest will be charged on such buying and selling for up to 3 days**. Even on the 3 rd day, all you have to do is sell your liquid fund and your account is settled immediately. So practically, you may never have to sell your cash position. All you have to do is to define how much of your capital would you want to keep in cash at any point, based on market factors.

** These margins and limits may vary. The above is based on the limits we provide to all our clients.

Now consider this:

If you choose an ultra-short to short term fund where interest rates are 8.9% – 9.6%, and can stay invested for up to 15 days, then you earn ~0.18 % on a weekly basis (provided that instead of 2-3 days, as above, you can plan your buying and selling for up to 15 days).

Depending on market factors you do get opportunities to invest in even higher interest bearing instruments. For now, if you are still worried about losing out on basic interest income in trading account and are constantly transferring money back and forth between your accounts, STOP. There are easier solutions in life and better things to do after 3.30 pm.

The original post is by Mastermind, Megabaggers and appears here.

I find it ironic that more research is being done today than at any point in time in the past, yet a lot of value investors are failing to beat the market.

Ironically, the mountain of articles on popular investing websites just aren’t helping. Part of the problem might be due to the “more brains” problem Graham cited years ago. Since everybody on Dalal Street is so smart, all those brains ultimately cancel each other out.

This glut of brain power, investment research, and investors clamouring for bargains does not mean that you can’t beat the market. But, knowing how to pick value stocks is a key requirement, along with having a good strategy and being prepared to do things that most other investors aren’t.

The Reserve Bank of India has recently announced how banks can be opened. This informative article has been authored by Mastermind, Deepak Shenoy. The original post appears here.

RBI will allow banks to be created “on tap” in the private sector. Meaning if you qualify, you can go apply for a licence – much like a driving licence – and get one. The previous model was: you waited till the RBI told you it wanted people to bid for a licence. This wait could be for 10 years. Then you applied and you waited, usually for two or three years. Then you were told that your fingernails were dirty and please clean them and reapply. And then you died and no one remembered you for it.

This post is authored by Mastermind, Deepak Shenoy and appears here.

Mauritius based entities that Invest in India – from Private Equity investors, VC funds, and investment pass-through vehicles (which issue participatory notes) will start to see taxation apply to them from April 1, 2017. This is due to a treaty change between India and Mauritius.

Currently, if you are a foreign investor, you can invest in Indian companies – both listed and unlisted. When you sell them, you would pay capital gains taxes in India (as many NRIs do) and some of those gains are withheld before you get the money.

The original article appears on www.rakesh-jhunjhunwala.in and is available here.

Time To Be Cautious & Raise Cash As Market Crash Is Imminent: Technical Analysis Expert

Nooresh Merani, a leading technical analysis expert, has issued a warning that the steep rally in stock prices is on the verge of reversing into a steep crash. He advises that we should exercise caution and take some money off the table so that we will have better buying power when the crash does come.

Common sense tells us that whenever there is a steep rally or a steep crash, there is always a reversal at some stage.

The original article appears on BloombergView and is available here. The author is Mark Buchanan.

Humans have a terrible track record of predicting financial crises in time to fend them off. Some computer scientists think that algorithms might help.

Given the right information, some crises can be foreseen. In “The Big Short,” Michael Lewis told the story of the scattered few who saw the imbalance growing in the mortgage market and profited as a result. Over decades, academic research has shown that many banking crises come with early warning signals, such as rapidly increasing debt and leverage. Yet economists and policy makers routinely miss such danger signs, in part because the financial world is so complex.

Peter Lynch (born January 19, 1944) is an American businessman and stock investor. As the manager of the Magellan Fund at Fidelity Investments between 1977 and 1990, Lynch averaged a 29.2% annual return,consistently more than doubling the S&P 500 market index and making it the best performing mutual fund in the world. During his tenure, assets under management increased from $18 million to $14 billion. He also co-authored a number of books and papers on investing and coined a number of well known mantras of modern individual investing strategies, such as Invest in what you know and ten bagger. Lynch is consistently described as a “legend” by the financial media for his performance record,and was called “legendary” by Jason Zweig in his 2003 update of Benjamin Graham‘s book, The Intelligent Investor.