Quantified trading signals can be based on different types of strategies. Some buy high in the hopes of selling higher, while others try to create a great risk/reward ratio by buying low hoping to sell on rebounds or reversals in price action. Here are four different types of trading signals.

Momentum signals are based on buying strength. Momentum traders wait for a strong move in a stock and then buy and get on-board for a short amount of time. Momentum traders usually trade short time frames of days. These work primarily in bull markets.

Breakout signals are based on buying all-time highs or 52 week highs, trying to buy high and sell higher. Breakouts are bought trying to catch a parabolic move where a stock could double or even triple over weeks and months. These work primarily in strong bull markets when indexes break to all-time highs.

Buying oversold dips are based on buying a long term price support level or an oversold oscillator like the 30 RSI, a price extension far from the 10 day EMA, or a -80 to -100 $NYMO. This signal tries to create a great risk/reward ratio based on buying a deep dip of a historical price range. These work best in range-bound markets.

Trend following signals try to go in the direction of the long term trend by using long term moving averages like the 200 day SMA breaks as buy or sell signals, or all-time highs or lows to enter longs or shorts. These work in trends with higher highs or lower lows.

The original article is authored by Steve and appears on New Trader U. It is available here.

Successful investors, being humans, can make mistakes too. However, it is the humbleness of these investors that make them successful, and George Soros put it best,

“I’m only rich because I know when I’m wrong…I basically have survived by recognizing my mistakes.”

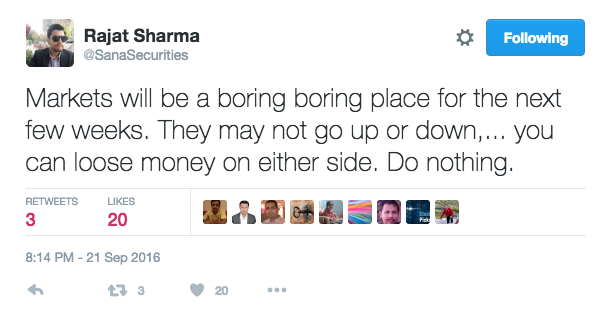

Over the past few months I have received many requests for portfolio rebalancing. Since August, I have been of the view that this is not the best time to deploy fresh capital in the market.

Those already invested should try to rebalance their portfolios and so I have done in many client folios.

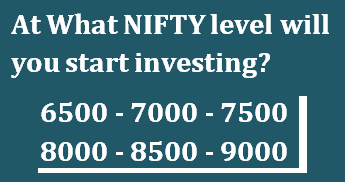

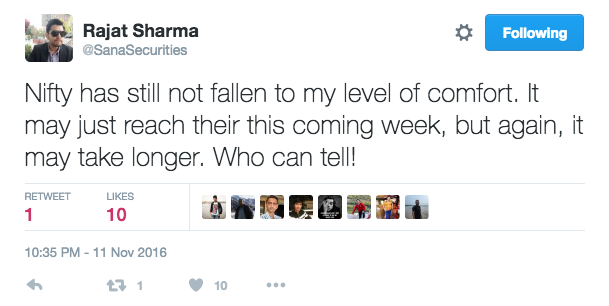

Common question: with NIFTY having fallen ~ 10% from its highs made earlier this year, is it time to start buying stocks? Here’s how valuations will look at different levels on the Nifty with current EPS base.

At what NIFTY level will you start investing?

7000

7500

8000

8500

9000

To calculate current EPS, I will be taking current Nifty P/E (15 November, 2016) which is 21.00.

P/E = Price (Nifty level)

Earnings per Share (EPS)

Current EPS = 379

[1] Nifty at 7,000 levels

P/E = 7,000/379

=18.47

[2] Nifty at 7,500 levels

P/E = 7,500/379

=19.79

[3] Nifty at 8,000 levels

P/E = 8,000/379

=21.11

[4] Nifty at 8,500 levels

P/E = 8,500/379

=22.45

[5] Nifty at 9,000 levels

P/E = 9,000/379

=23.75

CURRENT NIFTY PE AS OF 15 NOVEMBER 2016 = 21.37

VIEW

Typically, in a bull market (which I believe we certainly are in right now); valuations tend to run ahead of the earnings. It would be difficult to buy these markets at valuations of sub 19 level anytime soon. Further, some of the buying and selling that happened over the past 2-3 days has no explanation.

There sure is some amount of panic and herd selling. This could go on for some time as investors sell their liquid investments to arrange cash in the short term. Certainly with this new reality (of demonetization) one thing every investor should do is to pay some attention to his portfolio and rebalance it in light of the new realities.

As for buying stocks, sure . . . . . the tide could turn anytime from these levels.

The original post is written by Rajat Sharma of Mastermind, Sana Securities and is available here.

For a week now demonetization of high value notes has been polarizing the country between those who totally support the idea and those who are against it. The move has had a big impact on the stocks markets. A lot of investors are withdrawing capital from stocks. Some because they are out of funds (since the currency they had at home no longer works) and others because they expect a crash, perhaps an opportunity to buy at lower levels.

The government’s currency swap plan to withdraw Rs 500 and Rs 1,000 bank notes from circulation as a way to demonetise is being hailed by many banks and experts as the ultimate weapon against black money. However, demonetisation, as a strategy, isn’t new and has been tried before with limited success.

Here’s what former Reserve Bank of India governor Raghuram Rajan once said during a lecture on the topic of demonetisation and if it worked.

Rajan: I am not quite sure if what you meant is demonetise the old notes and introduce new notes instead. In the past demonetisation has been thought off as a way of getting black money out of circulation. Because people then have to come and say “how do I have this ten crores in cash sitting in my safe” and they have to explain where they got the money from. It is often cited as a solution. Unfortunately, my sense is the clever find ways around it.

They find ways to divide up their hoard in to many smaller pieces. You do find that people who haven’t thought of a way to convert black to white, throw it into the Hundi in some temples. I think there are ways around demonetization. It is not that easy to flush out the black money. Of course, a fair amount may be in the form of gold, therefore even harder to catch. I would focus more on the incentives to generate and retain black money. A lot of the incentives are on taxes.

My sense is the current tax rate in this country is for the most part reasonable. We have a reasonable tax regime, for example, the maximum tax rate on high-incomes is 33%, in the US it is already 39% plus State taxes, etc., it takes it to near 50. We are actually lower than many industrial countries. Given that, there is no reason why everybody who should pay taxes is not paying taxes. I would focus more on tracking data and better tax administration to get at where money is not being declared. I think it is very hard in this modern economy to hide your money that easily.

LalithDoshiMemorialLecture

The original article appeared in The Huffington Post and is available here.

In a 2000 article published in Money, Jason Jweig profiled a remarkable investor and friend of Warren Buffett named Joseph Rosenfeld who oversaw the investment committee for Grinnel College, a small school in Iowa.

“Joe,” says Buffett, “is a triumph of rationality over convention.” By ignoring the conventional wisdom about investing, Rosenfield has made money grow faster and longer than almost anyone else alive. Since 1968, he’s turned $11 million into more than $1 billion. He has heaped up those gains not with hundreds of rapid-fire trades but by buying and holding–often for decades. In 30 years, he’s made fewer than a half-dozen major investments and has sold even more rarely. [emphasis added] “If you like a stock,” says Rosenfield, “you’ve got to be prepared to hold it and do nothing.”

Here are the lessons from Joe Rosenfeld as summarized by Jason Jweig.

Do a few things well. Rosenfield built a billion-dollar portfolio not by putting a little bit of money into everything that looked good but by putting lots of money into a few things that looked great. Likewise, if you find a few investments you understand truly well, buy them by the bucketful. However, I think Rosenfield is a rare exception. Without his kind superior knowledge, skill and connections, most of us mere mortals need to diversify broadly across cash, bonds, and U.S. and foreign stocks.

Sit still. If you find investments that you clearly understand, hold on. Since it was their long-term potential that made you buy them in the first place, you should never let a short-term disappointment spook you into selling. Patience–measured not just in years but in decades–is an investor’s single most powerful weapon. Witness Rosenfield’s fortitude: In 1990, right after he bought Freddie Mac, the stock dropped 27%-. Rosenfield never panicked. Instead, he just waited. “Joe invests without emotion,” says Buffett, “and with analysis.

Invest for a reason. Rosenfield is a living reminder that wealth is a means to an end, not an end in itself. His only child died in 1962, and his wife died in 1977. He has given much of his life and all of his fortune to Grinnell College. “I just wanted to do some good with the money,” he says. That’s a lesson for all of us. Instead of blindly striving to make our money grow–or measuring our worth by our possessions–each of us should pause and ask: What good is my money if I never do some good with it? Is there a way to make my wealth live on and do honor to my name?

The original article is authored by Greg Speicher and appears on the blog here.

The decision by consulting major Capgemini to replace nearly 40% of its work done by its resource management group with IBM’s cognitive computing system, Watson, is a clear indication that it is not just repetitive or mechanical jobs that are at risk. Artificial intelligence (AI) is capable of taking on those tasks that require analytical skills. The tasks from education and skill development just got tougher.

By 2025, 70% of India’s population is projected to be of working age. A chunk of India’s present knowledge economy would have been chomped down by AI. As the knowledge economy evolves, India’s ability to continue playing a big role in that depends on swiftly raising the quality of education.

This article appears on valuewalk.com and can be found here.

Who Is Benjamin Graham?

History has designated Benjamin Graham as the Father of Value Investing. He not only developed the concept but also lived it, both as a practitioner with a remarkable track record and as a professor who profoundly impacted his students.

Among his many accolades, Father of Value Investing is Benjamin Graham’s greatest title. Some of his other designations are Dean of Wall Street and Dean of Security Analysis.

Father of Value Investing

His research paved the way for today’s stock market analysts by introducing the concept of fundamental analysis and raising awareness of the correlation between stock prices and a company’s intrinsic value.

Monster stocks are those wonderful beasts that make you look like a genius trader.

Shorts think that they are way too expensive and will crash, so they go short and have to cover en-mass after another 10 point run; they create even more buying pressure. Traders that short monster stocks do not understand the momentum that earnings expectations and growth cause for a stock’s price. They do not understand supply and demand. A stock that is $300, $400, or $500 based on earnings per share, could still be fundamentally cheaper than a $10 junk stock that has billions of shares floating around with tiny earnings per share.

PNB Housing Finance is entering the primary market on Tuesday 25th October 2016, to raise Rs. 3,000 crore, via a fresh issue of equity shares of Rs. 10 each, in the price band of Rs. 750 to Rs. 775 per share. Based on the price discovered, company will issue 3.9 to 4.0 crore equity shares at the upper and lower end of the price band respectively. Representing 23.37% of the post issue paid-up share capital at the upper end, issue closes on Thursday 27th October.

51% subsidiary of Punjab National Bank, PNB Housing Finance is India’s 5th largest home loan provider (after HDFC, LIC Housing, Dewan and Indiabulls Housing) with loan book of Rs. 30,900 crore (30-6-16), 70% of which is housing loans, having average ticket size of Rs. 32 lakh. Average ticket size for non-housing loans, which constitute 30% of the loan book, is Rs 57 lakh. With operations mostly in the urban areas of North, South and West India, its loan book has posted CAGR of 62% between March 2012 to June 2016.

While FY16 revenue grew 52% YoY to Rs. 2,700 crore, Net interest income (NII) jumped 63% YoY to Rs. 840 crore, leading to net profit of Rs. 328 crore and EPS of Rs. 27.58, on equity of Rs. 126.92 crore. Net interest margin (NIM) of 2.98% was clocked in FY16, up from FY15’s 2.94%, while Return on average assets (RoA) stood at 1.35%, up from FY15’s 1.27%.

The stupendous financial performance continued into FY17, with revenue of Rs. 863 crore, NII of Rs. 255 crore and net profit of Rs. 96 crore for the June quarter. Q1FY17 EPS stood at Rs. 7.57. Despite the phenomenal growth, asset quality is has remained intact, infact better than industry average. Gross NPAs, as of 30-6-16, of Rs. 84 crore, represents 0.27% of gross assets.

As of 30-6-16, company had networth of Rs. 2,240 crore, translating to BVPS of Rs. 177. It has only 2 shareholders – parent Punjab National Bank (51%) and Carlyle Group (49%), the latter pursuant to its acquisition of Destimoney Enterprises in Feb 2015. Fresh issue proceeds of Rs. 3,000 crore will augment company’s capital base. Current capital adequacy ratio (CAR) stands at 13.04% vis-à-vis regulatory requirement of 12%.

Given the room which fresh capital will provide the company for further leverage, capital being lifeline for any finance business, FY17 expected EPS is estimated at about Rs. 35 per share. At Rs. 775, company’s market cap will be Rs. 12,837 crore, upon listing, based on expanded equity of Rs. 165.63 crore. Estimated BVPS, as of 31-3-17, is Rs. 340, which translates into PBV multiple of 2.3x, while the PE multiple works out to 22x, based on current year estimates.

Below is a comparison with other listed housing finance companies, both bigger and smaller than the company:

Company Name

(Rs. Crore)

Loan Assets

Revenue

PAT

Gross NPA %

Current Market Cap

Mcap % to loan assets

PE

PBV

As of 30-6-16

QoQ Growth

FY16

YoY growth

FY16

YoY growth

Margin

30-6-16

FY17E

FY17E

LIC Housing

1,27,437

1.8%

12,396

16.2%

1,661

19.8%

13.4%

0.59%

31,087

24%

16.9x

2.8x

Dewan

72,012

3.6%

7,312

22.2%

729

17.4%

10.0%

0.98%

10,455

15%

11.6x

1.7x

Indiabulls Housing

71,026

3.4%

8,290

28.2%

2,345

23.4%

28.3%

0.84%

37,121

52%

12.5x

2.7x

PNB Housing

30,901

13.7%

2,700

51.6%

328

68.9%

12.1%

0.27%

12,837*

42%*

22.1x*

2.3x*

Gruh Finance

11,543

3.9%

1,275

20.3%

244

19.5%

19.1%

0.56%

12,409

108%

44.3x

11.1x

Can Fin

11,183

5.1%

1,084

32.6%

157

82.1%

14.5%

0.24%

4,861

43%

22.1x

4.3x

* at upper end of price band of Rs. 775 per share

The growth rates which PNB Housing has posting is the highest in the industry (only Can Fin reported higher PAT growth in FY16, but its revenue and loan book growth was much lower). Moreover, PNB Housing’s NPAs have also been under check – 2nd best in the peer set. While net margins and RoE can improve further, based on valuation parameters of PBV multiple (2.3x) and market cap as a % to loan assets (42%), the pricing of the issue appears in-line. Growth visibility in the stock remains very high, given the fresh capital coming into the business, which provides added comfort.

Housing finance industry has been on a growth trajectory, with further headroom for growth. Company’s industry-leading growth coupled with sound fundamental position make it an attractive investment opportunity, albeit softening due to higher base.

Positive sector outlook coupled with stunning growth rates make the issue a subscribe.

Disclosure: No Interest.

The original article is authored by Geetanjali Kedia and is available here.

and Dean of Security Analysis

and Dean of Security Analysis .

.