Reblog: One Million Market Beaters

The article is written by Michael Batnick, CFA, Director of Research at Ritholtz Wealth Management. The original article appears here.

Uncertainty remains, but Florida is in the cross hairs.

What to expect today after tornado outbreak.

Why we’re watching Gaston closely now.

These headlines were pulled from a few articles today at weather.com. You could seamlessly replace Florida, tornado, and Gaston with a stock because like the weather, markets are highly complex with countless variables that can’t fully be modeled.

In his highly entertaining book, But What If We’re Wrong, Chuck Klosterman talks about how much money has been spent trying to predict the weather:

Somebody once told me a joke about meteorology. The premise is that we’ve been trying to predict the weather since 3000 BC. The yearly budget for the National Weather Service is $1 billion…Even a conservative estimate places the annual amount of money spent on meteorology at somewhere around $5 billion. And as a result of this investment, our weather can be correctly predicted around 66 percent of the time. As a society, we can go two out of three. Yet if some random dude simply says, “I think the weather tomorrow will be the same as the weather today,” he will be right 33 percent of the time. He can go one for three. So we’ve invested hundreds of billions of dollars and countless hours into meteorological research, with the net effect of becoming twice as accurate as some bozo who looks out the window and points at the sky.

The Wall Street Journal just reported that U.S. mutual funds spend more than $300 million every year to send investors written reports. This is an astonishingly large number, but it’s peanuts compared to how much they spend trying to beat their benchmark. And while the net effect of becoming twice as accurate as some bozo might be true with the weather, it’s the opposite with investing.

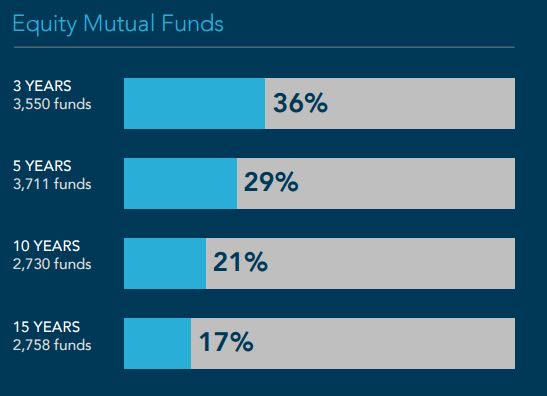

The chart below from Dimensional Funds shows that all a bozo has to do to beat the majority of professionals is buy an index fund.

There are a number of explanations as to why funds underperform, from high-fees to tax inefficiencies to the high level of competition and so on. But the simplest explanation as to why so many mutual funds fail to beat an index is because so many stocks fail to beat the index.

J.P. Morgan and Longboard Asset management both have done great work on how difficult stock picking is. Below are some of their findings.

- 25% of stocks accounted for all of the markets’ gain.

- 40% of all stocks suffer a catastrophic loss (70%) and never fully recover.

- The median stock underperformed the market with an excess lifetime return of -54%

- Two-thirds of all stocks underperform the market.

- 40% of all stocks have negative total returns.

- 18.6% of all stocks dramatically underperform the market.

- 53% of all technology stocks have had negative returns.

- Since 1980, over 320 stocks were removed from the S&P 500 due to distress.

- Evert sector had a negative median excess return versus the market.

- Only 6.1% of stocks dramatically outperformed the market during their lifetime.

In 2015, there were 99 million global stock trades a day to the tune of $498 billion. That’s a lot of people who all share the same goal of buying stocks that are going to outperform. I know we all think statistics don’t imply to us, but they really do. According to a 2013 Deloitte study, 17 million Americans in the United States have a brokerage account. If just 5.9% of these 17 million beat the market, some lucky and some skilled, that’s 1,000,000 people. Chances are you know one of these people and think if they can do it, so can I. And you’d be right, you can do it, but the odds aren’t in your favor.

Source:

But What If We’re Wrong? Thinking About the Present As If It Were the Past