The first part of this post appears here.

Graham Number, an Introduction:

There are different ways of checking if a stock is undervalued at its current price, one of them and largely used is graham number. Graham Number is derived through a mathematical calculation to figure out the discount for any stock. Though it doesn’t work much for new age industries, branded plays, however consider this as a must check before investing into any stock. Sometimes this helps to build conviction too.

What is the ‘Graham Number’?

The Graham number is a figure that measures a stock’s fundamental value by taking into account the company’s earnings per share and book value per share. The Graham number is the upper bound of the price range that a defensive investor should pay for the stock. According to the theory, any stock price below the Graham number is considered undervalued, and thus worth investing in. The formula is as follows:

Breaking Down ‘Graham Number’

The Graham number is named after the “father of value investing,” Benjamin Graham. It is used as a general test when trying to identify stocks that are currently selling for a good price. The 22.5 is included in the number to account for Graham’s belief that the price to earnings ratio should not be over 15 and the price to book ratio should not be over 1.5 (15 x 1.5 = 22.5). It does leave out many fundamental characteristics which make up a good investment, and is not effective for the majority of medium- to large-cap stocks.

For example, if the earning per share is $1.50, book value per share is $10, the Graham number would be 18.37. If the stock price is $16, you should buy the stock as it is seen to be undervalued.

Why Graham Created This Valuation Formula

It’s no secret that Graham was a cheap stock investor who bought baskets of stocks instead of concentrating.

His approach was much mechanical.

His first criterion was cheapness and that was usually enough. But after going through countless stocks, here’s what he says.

Our study of the various methods has led us to suggest a foreshortened and quite simple formula for the valuation of growth stocks, which is intended to produce figures fairly close to those resulting from the more refined mathematical calculations. – The Intelligent Investor

In 3 short bullets, he used the formula himself for;

- Shorthand

- Simplicity

- Estimate of intrinsic value

It’s definitely not the golden rule and it’s not something he went with blindly, but it’s a good approximation and a good starting point to use in your investigation.

After all, Buffett says that

It is better to be approximately right, than precisely wrong.

The original post appears on ride2rich.com by Mastermind and is available here.

Probably the most important part of investing is to understand the valuation of a company. A good understanding of valuation gives immense confidence to investors to buy and sell stocks in every opportunity of under and over valuation. It is that magic wand in investors hand that helps them to pick up an undervalued stock or average a falling stock with great confidence. Valuation is the only parameter of utmost importance for investors that should guide them for entry, exit and holding strategies leading to dynamic portfolio management.However, as all important things in life, valuations of a stock too, is a difficult nut to crack.

There are many complex mathematical formulas available like DCF and reverse DCF , which tries to assign an intrinsic value | fair value of a stock by projecting in the future earnings from the business. However, they only work in ideal case scenario (*Considering everything else remains the same! ), which is never a reality given the dynamic nature of today’s businesses. So, valuing a company is a tricky job and requires a lot of understanding about different industries and the company to develop a qualitative understanding of about the valuation of the company under consideration. So, valuation today is more of a qualitative understanding and a gut feeling with a bit of stretching of imagination. It works to the level to understand if the stock is undervalued or overvalued or fairly valued to a great extent.

But to develop that understanding an investor got to look at different data points systematically to arrive at a conclusion about the valuation. In this blog series of understanding company valuations, I’ll systematically take up different parameters one needs to look into, to develop the most important ‘gut feel’ about the stock.

The first should be to understand the concept of Market values Vs Book Value in greater details. We will deal with that in this blog post.

Market Values Vs Book Value

Understanding the difference between book value and market value is a simple yet fundamentally critical component of any attempt to analyze a company for investment. After all, when you invest in a share of stock or an entire business, you want to know you are paying a sensible price.

Book value literally means the value of the business according to its “books” or financial statements. In this case, book value is calculated from the balance sheet, and it is the difference between a company’s total assets and total liabilities. Note that this is also the term for shareholders’ equity. For example, if Company XYZ has total assets of Rs.100 and total liabilities of Rs. 80 , the book value of the company is Rs. 20. In a very broad sense, this means that if the company sold off its assets and paid down its liabilities, the equity value or net worth of the business, would be Rs.20

Market value is the value of a company according to the stock market. Market value is calculated by multiplying a company’s shares outstanding by its current market price. If Company XYZ has 10 shares outstanding and each share trades for Rs.50, then the company’s market value is Rs.500 . Market value is most often the number analysts, newspapers and investors refer to when they mention the value of the business.

Implications of Each

Book value simply implies the value of the company on its books, often referred to as accounting value. It’s the accounting value once assets and liabilities have been accounted for by a company’s auditors. Whether book value is an accurate assessment of a company’s value is determined by stock market investors who buy and sell the stock. Market value has a more meaningful implication in the sense that it is the price you have to pay to own a part of the business regardless of what book value is stated.

As you can see from our fictitious example from Company XYZ above, market value and book value differ substantially. In the actual financial markets, you will find that book value and market value differ the vast majority of the time. The difference between market value and book value can depend on various factors such as the company’s industry, the nature of a company’s assets and liabilities, and the company’s specific attributes. There are three basic generalizations about the relationships between book value and market value:

- Book Value Greater Than Market Value: The financial market values the company for less than its stated value or net worth. When this is the case, it’s usually because the market has lost confidence in the ability of the company’s assets to generate future profits and cash flows. In other words, the market doesn’t believe that the company is worth the value on its books. Value investors often like to seek out companies in this category in hopes that the market perception turns out to be incorrect. After all, the market is giving you the opportunity to buy a business for less than its stated net worth.

- Market Value Greater Than Book Value: The market assigns a higher value to the company due to the earnings power of the company’s assets. Nearly all consistently profitable companies will have market values greater than book values.

- Book Value Equals Market Value: The market sees no compelling reason to believe the company’s assets are better or worse than what is stated on the balance sheet.

It’s important to note that on any given day, a company’s market value will fluctuate in relation to book value. The metric that tells this is known as the price-to-book ratio, or the P/B ratio:

P/B Ratio = Share Price/Book Value Per Share

(where Book Value Per Share equals shareholders’ equity divided by number of shares outstanding)

So one day, a company can have a P/B of 1, meaning that BV and MV are equal. The next day, the market price drops and the P/B ratio is less than 1, meaning market value is less than book value. The following day the market price zooms higher and creates a P/B ratio of greater than 1, meaning market value now exceeds book value. To an investor, whether the P/B ratio is 0.95, 1 or 1.1, the underlying stock trades at book value. In other words, P/B becomes more meaningful the greater the number differs from 1. To a value-seeking investor, a company that trades for a P/B ratio of 0.5 implies that the market value is one-half of the company’s stated book value. In other words, the market is selling you each Rs.1 of net assets (net assets = assets – liabilities) for 50 paise. Everyone likes to buy things on sale, right?

Which Value Offers More Value?

So which metric – book value or market value – is more reliable? It depends. Understanding why is made easier by looking at some well-known companies.

Page Industries Ltd.

Page has historically traded at a P/B ratio of 20+. This means that Page’s market value has typically been 20 times larger than the stated book value as seen on the balance sheet. In other words, the market values the firm’s business as being significantly worth more than the company’s value on its books. You simply need to look at their income statement to understand why. Page is a very profitable company. Its net profit margin exceeds 12%. In other words, it makes at least 12 paise of profit from each rupee of sales. The takeaway is that Page has very valuable assets – brands, distribution channels,Loyal customers- that allow the company to make a lot of money each year. Because these assets are so valuable, the market values them far more than what they are stated as being worth from an accounting standpoint.

Another way to understand why the market may assign a higher value than stated book is to understand that book value is not necessarily an accurate value of a company’s net worth. Book value is an accounting value, which is subject to many rules like depreciation that require companies to write down the value of certain assets. But if those assets are consistently generating greater profit, then the market understands that those assets are really worth more than what the accounting rules dictate.

State Bank of India:

SBI is one of the oldest and largest banks in the India. It typically trades for a P/B of around 1, give or take a few percent. In other words, the market values SBI at or close to its book value. The reason here is simple, and it is explained by the industry SBI operates in. Financial companies hold assets that consist of loans, investments, cash and other financial securities. Since these assets are made of Rupees, it’s easy to value them: a rupee is worth a rupee. Nothing more, nothing less. Of course we know that some financial assets can be better than others; for example, a good loan versus a bad loan. That’s why whenever banks experience a financial crisis, as we saw in the subprime meltdown in 2008, their market values crash below book value. The market loses faith in the value of those assets.

On the other hand, financial institutions like HDFC Bank, which have a long history of extending out good credit, will trade at a modest premium to book value (only around 3+). Banks that the market views as having made bad credit decisions will trade below book. But in general terms, you will never see banks trading for multiples of book value like you would see in Page Industries, because of the nature of their assets in their books. You may financially account for a money value of the same for both, however their nature is never the same.

When the Values Matter

To determine how book value relates to market value, look at the income generated by the company’s assets. A company than can generate a relatively high income level from its assets will typically possess a market value that’s far higher than its book value. This is called the company’s return on assets, or ROA. Page Industries ROA is typically around 40% and around 6% for SBI. This means each Rupee of Page Industries assets generates 40 paise of profit, whereas for SBI it is just 6 paise. So, market has a very valid reason for paying a high value for Page and not SBI.

What this also means is that in the case of companies like Page Industries, book value is not as meaningful as it would be for a company like SBI.

The Bottom Line

Book value, like almost all other financial metrics, has its usefulness. But as is often the case with financial metrics, the real utility comes from understanding the advantages and limitations of book value. An investor must use that understanding to determine when book value should be used, and when it should be disregarded in favor of other meaningful parameters when analyzing a company.

In my next posts on this ‘Valuation Series’ I’ll talk about other such important parameters to look at to develop the understanding of stock valuations.

The original post appears on ride2rich.com by Mastermind and is available here.

Credit monitoring firm Equifax recently reported that the issuance of consumer credit has risen to a six-year high. This could be a sign that the economy is finally getting back to normal, but it also could be a cautionary signal.

According to Equifax, the number of new credit cards issued is up 18.5 percent year-over-year, and the number of new auto loans originated is up 11.9 percent. An optimist might refer to this as the rebuilding of consumer credit, but that rebuilding is happening on a shaky foundation. Some people are taking on more debt without having paid down what they already owed, which could be a recipe for disaster.

Remembering the lean years

You can’t do anything about debt conditions in this country generally, but as the economic mood turns from pessimism to optimism, there are some personal finance lessons you should remember from the hard times of the past several years:

- Don’t get carried away with optimism. If you are feeling better about the economy and think you can afford to spend more, that’s great — as long as you are earning what you spend, not borrowing it. Ask yourself this: If you have to rely on borrowing to spend more, can you really afford it?

- You need to keep feeding your retirement account. Some great investment returns over the past few years have restored many retirement balances to health. Still, don’t take that as a cue to cut back on your contributions and let the markets do all the work. There may be some lean investment years somewhere along the way, and the best way to mitigate market setbacks is to keep steady additions going into your account.

- An emergency fund can come in handy. Besides saving for retirement, what many people learned from the aftermath of the Great Recession is that an emergency fund can be a necessity during hard times. Of course, when times get tough you don’t have the opportunity to build up this kind of reserve, so you have to remember to do it when things are going well.

- Checking account fees can bleed you dry. The financial crisis changed the fee environment for checking accounts, and even as conditions improve that environment has not been changing back. Free checking is harder to find, and overdraft fees have risen. By shopping around you can still find free checking accounts, and by opting out of overdraft protection you can develop better banking habits that will save you from those fees.

- Savings accounts may be dull, but they are not all the same. Somewhere around the time when savings account interest rates dropped below 1 percent, most people completely lost interest in them. However, those rates still vary greatly from bank to bank, so shopping around is as important as ever.

- Good jobs are hard to find. Employees may find themselves a little more in demand now, but they should never forget what it is like to be looking for a job in a soft economy. Keep your skills up to date, and never lose sight of how you can add value to your employer.

Optimism is great — it is necessary for a dynamic economy. However, after all people have been through since 2008, it would be better if that optimism were informed by some hard-earned wisdom.

Richard Barrington has earned the CFA designation and is a 20-year veteran of the financial industry.

This article was authored by Richard Barrington and originally published on www.deseretnews.com. It is available here.

Over the past few months I have received many requests for portfolio rebalancing. Since August, I have been of the view that this is not the best time to deploy fresh capital in the market.

Those already invested should try to rebalance their portfolios and so I have done in many client folios.

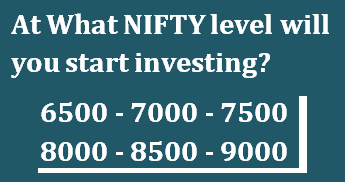

Common question: with NIFTY having fallen ~ 10% from its highs made earlier this year, is it time to start buying stocks? Here’s how valuations will look at different levels on the Nifty with current EPS base.

At what NIFTY level will you start investing?

To calculate current EPS, I will be taking current Nifty P/E (15 November, 2016) which is 21.00.

P/E = Price (Nifty level)

Earnings per Share (EPS)

Current EPS = 379

[1] Nifty at 7,000 levels

P/E = 7,000/379

=18.47

[2] Nifty at 7,500 levels

P/E = 7,500/379

=19.79

[3] Nifty at 8,000 levels

P/E = 8,000/379

=21.11

[4] Nifty at 8,500 levels

P/E = 8,500/379

=22.45

[5] Nifty at 9,000 levels

P/E = 9,000/379

=23.75

CURRENT NIFTY PE AS OF 15 NOVEMBER 2016 = 21.37

VIEW

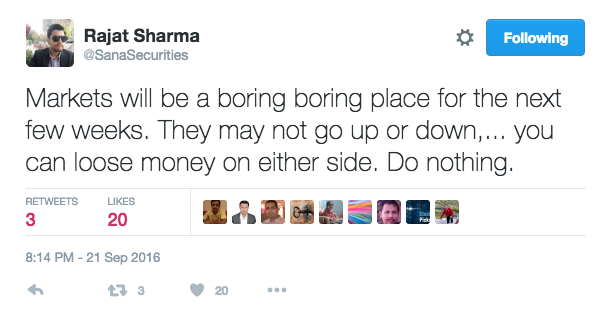

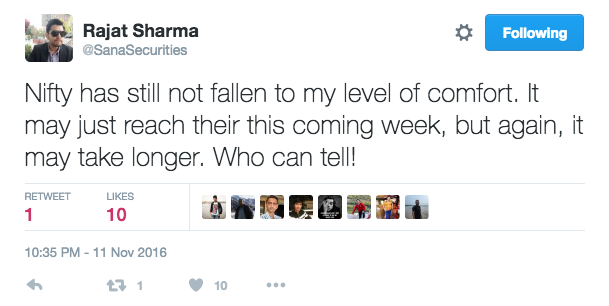

Typically, in a bull market (which I believe we certainly are in right now); valuations tend to run ahead of the earnings. It would be difficult to buy these markets at valuations of sub 19 level anytime soon. Further, some of the buying and selling that happened over the past 2-3 days has no explanation.

There sure is some amount of panic and herd selling. This could go on for some time as investors sell their liquid investments to arrange cash in the short term. Certainly with this new reality (of demonetization) one thing every investor should do is to pay some attention to his portfolio and rebalance it in light of the new realities.

As for buying stocks, sure . . . . . the tide could turn anytime from these levels.

The original post is written by Rajat Sharma of Mastermind, Sana Securities and is available here.